Islamic fintech does not lack narrative or ambition.

There are two billion potential Muslim customers globally. Islamic finance assets exceed $6 trillion. Markets across the GCC and Southeast Asia combine strong banking penetration with rising digital adoption. Diaspora markets like the UK remain structurally underserved.

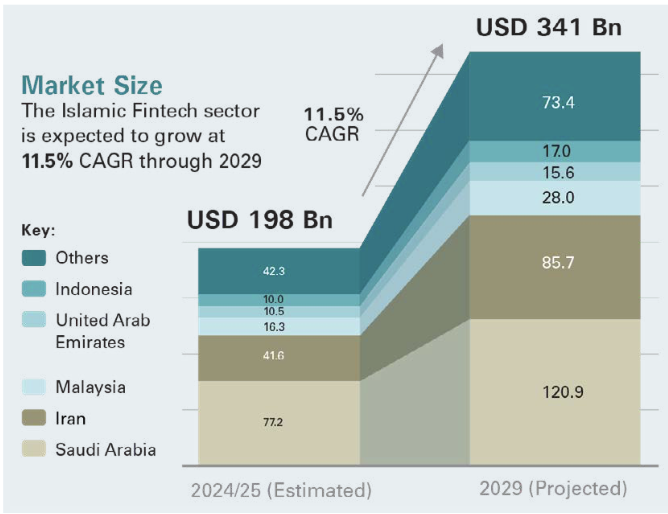

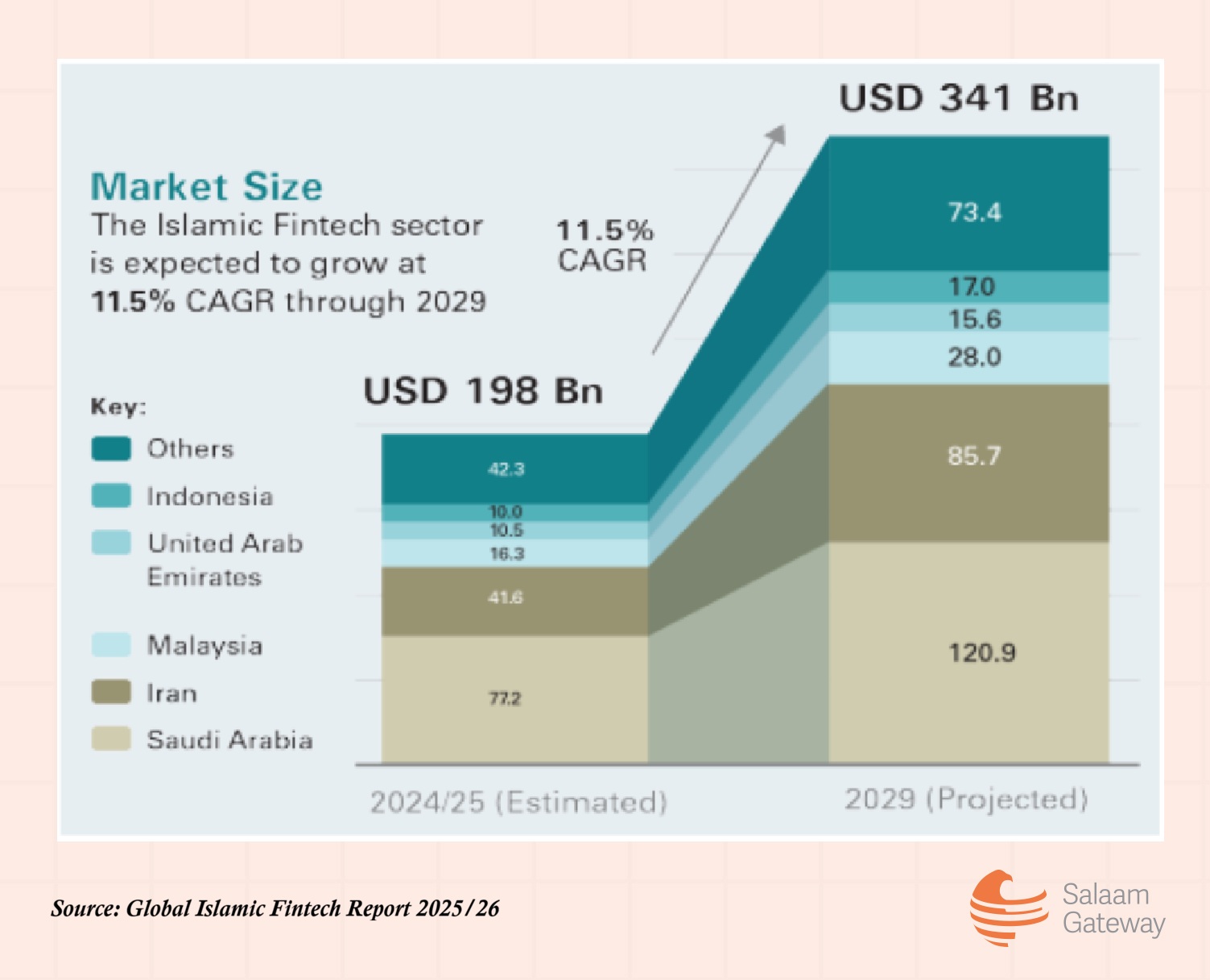

The Global Islamic Fintech Report 2025/26 estimates the size of Islamic fintech at $198 billion, projected to reach $341 billion by 2029. There are 484 Islamic fintech firms worldwide, concentrated largely in alternative finance, wealth management, payments, deposits and lending. Digital assets, takaful and social finance remain less developed but show momentum.

Yet despite these tailwinds, Islamic fintech still represents just 1.5% of the global fintech market.

The opportunity and growth are clear, but capital remains selective.

Not always a venture case

Venture capital is often the first route founders consider when raising funding. But Abdul Haseeb Basit, co-founder and principal of Elipses, suggests the sector needs to think more carefully about fit.

“Mostly, Islamic finance products require patience and development. They don't have the same turnaround times as conventional venture investments, so it requires a type of patient capital that perhaps isn't venture capital.”

Islamic finance is rooted in asset-backing, risk-sharing and structured governance. That does not always align neatly with venture capital’s expectation of rapid scaling and defined exit timelines.

Hazem Ben-Gacem, founder and chief executive of BlueFive Capital, agrees that venture capital is only one tool. His firm led Mal’s $230 million seed round, backing what it describes as the world’s first AI-native Islamic digital bank. The investment demonstrates that institutional capital is prepared to move at scale when conviction is strong.

“VC works well for high-growth, scalable platforms, which is why we led this round for Mal,” he says. “But Islamic finance is fundamentally rooted in asset-backing, risk-sharing and ethical allocation of capital. That aligns more naturally with revenue-based financing, sukuk, or even crowdfunding in certain contexts. We need a hybrid approach.”

Wahed offers another example. The US-based Islamic robo advisory platform has raised multiple rounds to expand across the US, UK and MENA markets. Licensing friction did not deter investors because the underlying business model scaled and governance structures were clear.

These examples show Islamic fintech can attract venture funding. The issue is that only specific models fit the venture profile.

Going beyond faith positioning

Islamic fintech combines digital infrastructure with principles such as asset-backing, transparency and risk-sharing. Shariah compliance matters to customers. Investors, however, assess propositions differently.

Khalid Howladar, managing partner at advisory and venture firm Acreditus, argues that targeting underserved Muslim communities can be commercially logical at the outset.

“As long as your project can make money serving this segment, venture capital will follow,” he says.

However, Howladar adds a crucial caveat. “Focusing on community is not enough. Just being Islamic is not enough. You need to be solving a problem, ensuring product market fit.”

Basit echoes this point. He believes founders need to broaden their lens. “Most of the development today has been around structuring the products in a Shariah-compliant way. Now the focus needs to shift to their merits as an investment product more holistically.”

To scale, Islamic fintech must demonstrate that it delivers better financial outcomes, not simply compliant alternatives.

The firms attracting capital tend to compete on commercial fundamentals first, with Shariah embedded in governance rather than positioned as the sole differentiator.

Product diversity and scalability

The Global Islamic Fintech Report highlights the heavy concentration of firms in retail-facing segments such as payments and wealth management. These areas are important but can be geographically constrained and highly competitive.

Greater product diversity is needed, such as digital asset rails aligned with asset-backing principles; capital markets technology; embedded Islamic finance within broader ecosystems; SME financing platforms with scalable underwriting models. These types of propositions are more likely to scale across markets and attract institutional capital.

Ben-Gacem argues Islamic fintech remains underfunded relative to its structural opportunity.

“The challenge has been twofold,” he says. “First, many solutions have been reactive - digitising conventional Islamic products rather than reimagining them. Second, the investor base has been too narrow. We see this as a gap in perception, not performance. What’s been missing is conviction at scale.”

Investors have shown greater willingness to back regulated infrastructure than narrowly positioned consumer applications. That distinction is likely to shape future deal flow.

A shallow capital escalator

Even where early-stage capital exists, scaling remains uneven.

Basit describes what he calls a weaker “capital escalator”. Incubators and angel networks are active. However, later-stage funding remains limited.

He notes that corporate venture participation from Islamic banks is not yet widespread, and IPO pathways for high-growth technology firms in many OIC markets are still developing.

Without visible late stage exits, institutional LPs hesitate to allocate capital to specialised Islamic fintech funds. Without larger funds, scaling beyond Series A or B becomes difficult.

“There needs to be a whole-of-ecosystem approach when it comes to funding a company from inception to exit,” adds Basit.

“We haven't seen much later-stage scaling. We have seen some exits, for example CoinMENA was a trade sale. That is probably likely to be the most common outcome for most Islamic fintechs.”

Governance and interpretation risk

Another friction point lies at the intersection of Shariah governance and venture structuring.

Amjad Hussain, partner at law firm K&L Gates in Qatar, notes that founders sometimes focus on Shariah compliance at the product level while relying on conventional funding instruments at the equity level.

“Early funding continues to be raised through conventional instruments that are drafted in a debt-like or return-protective nature,” he says. “Convertible notes, for example, are typically framed as debt that converts into equity and often include an interest component, which is an obvious friction point in a Shariah context.”

Hussain argues that Shariah governance should be embedded from the outset, with “instrument choice, conversion mechanics and investor protections aligned from the first term sheet”.

At the same time, he cautions against overcorrecting.

“The aim is not to reinvent venture economics, but to express them in equity-forward terms that are commercially familiar and Shariah-compliant.”

Consistency is key

Islamic fintech benefits from favourable structural trends. Demand is robust. Regulatory clarity in markets such as Malaysia and parts of the GCC is improving.

But venture capital is not unlocked by narrative alone. It requires scalable business models, disciplined governance, predictable regulatory planning and credible exit pathways.

Islamic fintech has demonstrated that capital can be raised. The challenge is not promoting an outlier. It is making it the norm.