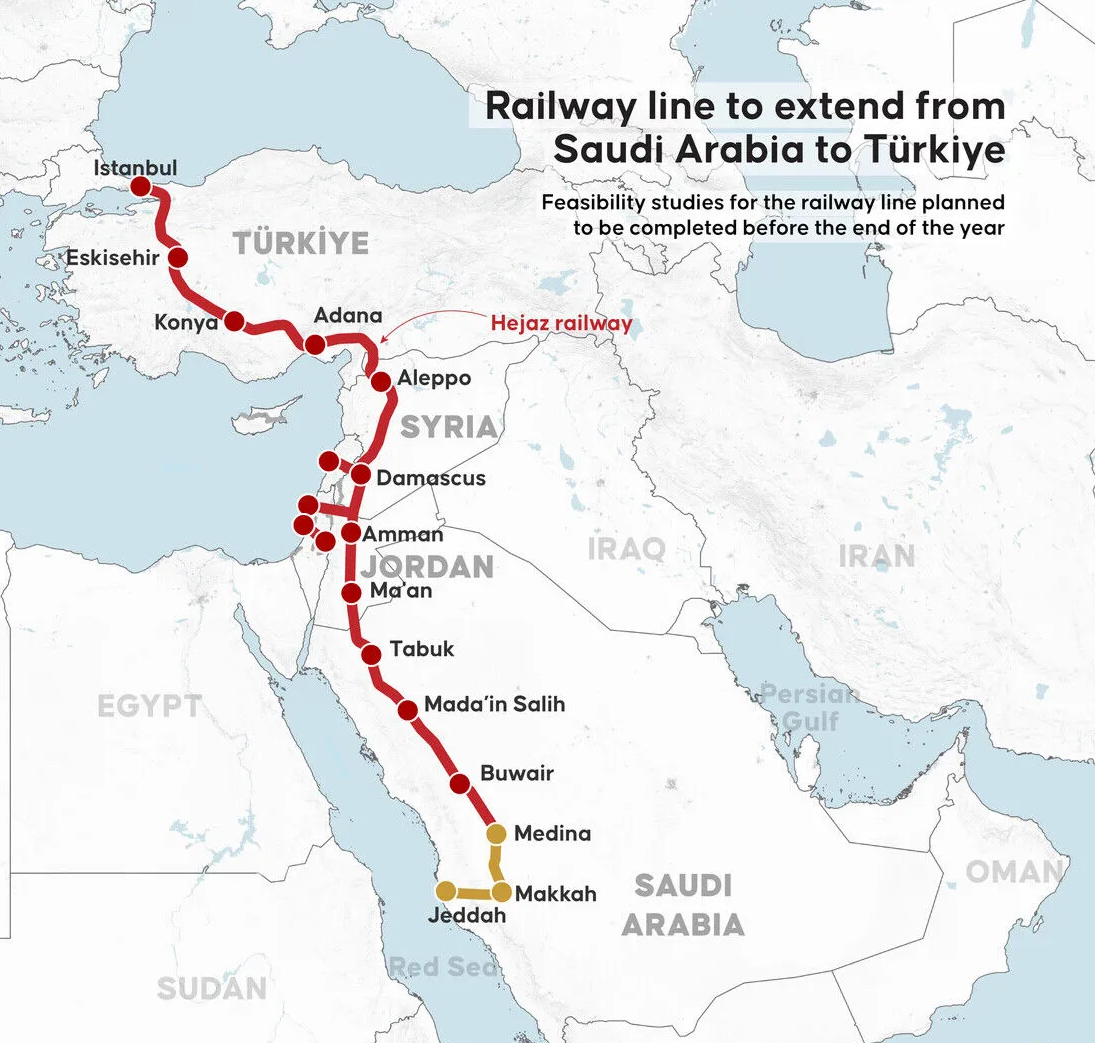

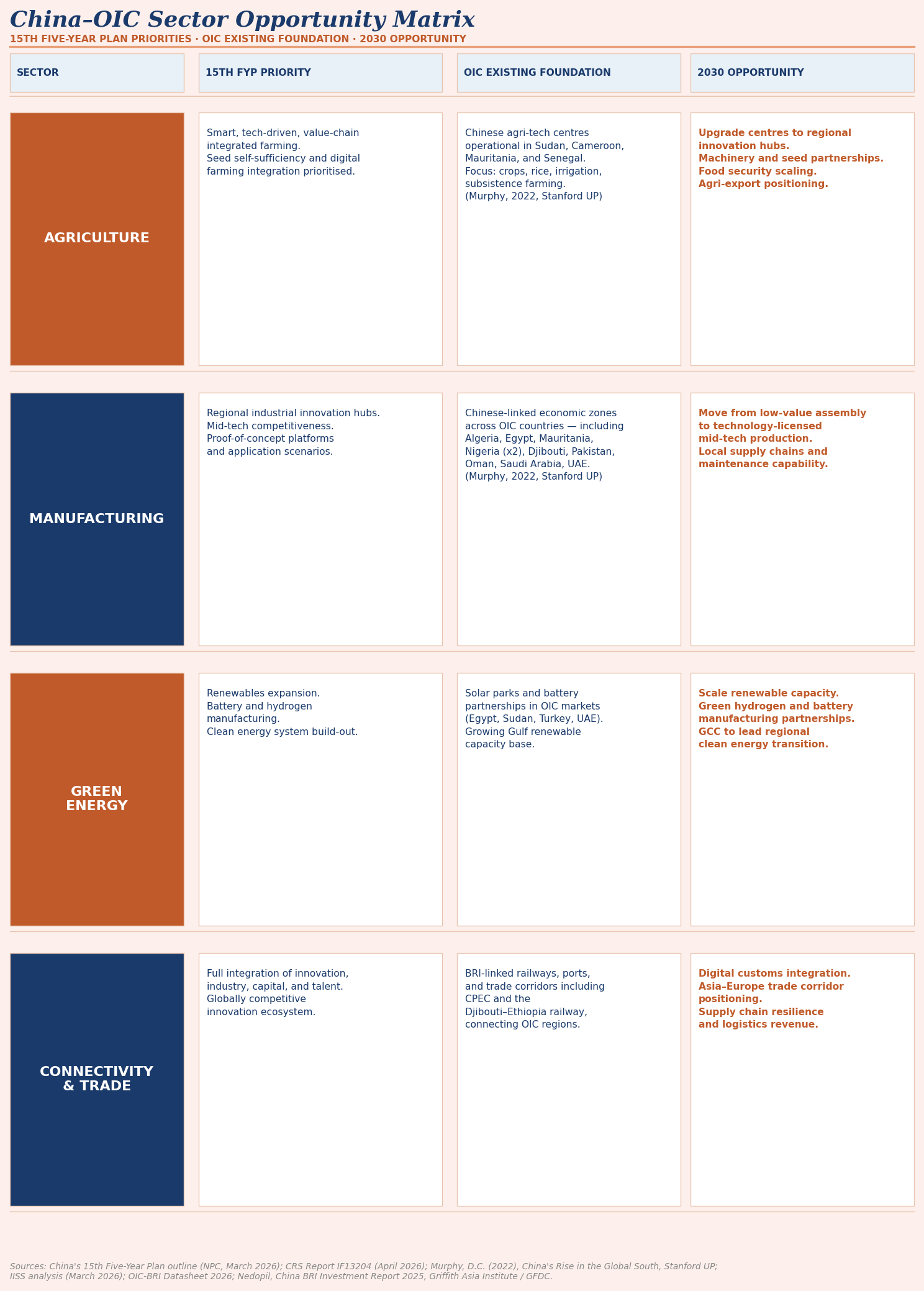

The newly signed railway cooperation agreement between Türkiye and Saudi Arabia could pave the way for one of the most ambitious geo-economic corridors in the Islamic world. Designed to connect the two countries via Jordan and Syria over the next three to four years, the architecture promises to secure regional supply chains and reduce dependence on volatile maritime chokepoints by ultimately establishing an overland trade route linking the Gulf to Europe.

While the memorandum of understanding is still in its early stages, analysts agree that the project's significance extends far beyond transportation. It reflects a changing Middle East where infrastructure is increasingly seen as a source of geopolitical influence, strategic resilience, and regional integration.

Source: Anadolu Agency

This rail pact is part of a larger trend of growing collaboration between the two nations, arriving on the heels of a recent MoU between the Saudi Food and Drug Authority and the Turkish Halal Accreditation Agency to advance joint research, training, and development in the halal sector.

Born from geopolitical shifts, morphed into economic resilience

The timing of the initiative is no accident. Years of conflict across Middle Eastern countries, coupled with repeated disruptions to global shipping and growing anxieties over the Strait of Hormuz, have accelerated interest in alternative overland trade routes.

According to Turkish Transport Minister Abdulkadir Uraloğlu, the proposed network is designed to create a flexible logistics web capable of adapting to regional instability, rather than relying on a single, vulnerable trade artery.

Geopolitical analyst James M. Dorsey notes that this announcement reflects a broad Middle Eastern transformation: "A Turkish-Saudi agreement to revive the Ottoman-era Hijaz Railway tells the story of geopolitical realignment in the wake of the wars in Gaza, Lebanon and Iran."

However, despite comparisons to the original Hejaz Railway, experts argue that the similarities end with geography. While the Ottoman system primarily transported pilgrims along a north-south axis, the new corridor is designed to move manufactured goods, industrial inputs, agricultural products, and investment capital across Europe, the Middle East, and Asia.

Majed Elmedawar, a strategic adviser specializing in Middle Eastern economic integration, emphasizes that modern railways should be viewed as economic institutions.

He stresses that the bilateral initiative is part of a sweeping regional infrastructure push that includes the planned 2,177-kilometer GCC Railway, Iraq's $17 billion Development Road project connecting the Gulf to Türkiye, and the India-Middle East-Europe Economic Corridor (IMEC) announced in 2023.

"The Türkiye-GCC railway should be understood not as a revival of the historic Hejaz Railway but as a fundamentally different category of infrastructure,” Elmedawar notes.

“Infrastructure does not only connect economies; it creates economies. A railway corridor generates industrial clusters, logistics hubs, manufacturing links, labor mobility, investment concentration, and urban growth."

What does it mean for OIC countries & the broader Islamic economy

Perhaps the project's greatest promise lies in what analysts call cooperative sovereignty. Rather than diluting national independence, shared infrastructure can strengthen it. By managing transnational flows of goods and capital, states can participate in the global economy from a position of strength.

For members of the Organization of Islamic Cooperation (OIC), this means replacing reliance on vulnerable shipping routes with robust, localized supply chains. Countries located directly along the corridor - including Türkiye, Saudi Arabia, Jordan, and eventually Syria - would likely see the greatest immediate benefits through expanded logistics industries, manufacturing investment, and tourism, according to Elmedawar.

Longer-term, the network could extend commercial opportunities to Egypt, Pakistan, Central Asia, and Southeast Asian nations through wider Eurasian transport links.

One of the most transformative impacts of the corridor could be on the rapidly expanding halal economy, which now encompasses pharmaceuticals, cosmetics, finance, and tourism. Currently, fragmented transport systems inflate costs and bottleneck trade between OIC markets.

A modernized rail network has the potential to change this by offering reduced transit times for perishable halal goods, providing temperature-controlled freight movement combined with digital tracking, and encouraging harmonized certification systems across borders.

"A halal-certified product is only as competitive as its ability to reach consumers at a reasonable price and in a timely manner," Elmedawar notes.

Integrated rail would turn isolated national markets into a massive, interconnected halal industrial cluster. Beyond trade, the project carries significant cultural and diplomatic implications. Ahmet Akalin, assistant director at the Iran-based Economic Cooperation Organization Cultural Institute, sees transportation as a crucial tool for international influence.

By reducing logistical barriers, Akalin argues, the corridor would reinforce Türkiye's role as a strategic bridge between Europe, Asia, and the Arab world while bolstering regional cooperation. Furthermore, he believes the railway may become the backbone of a trusted halal logistics network.

Drawing on insights from his book, The Appeal of Nations - International Cultural Institutes in Türkiye in the Context of Soft Power, he notes that the halal industry extends beyond mere religious compliance. “Halal also represents hygiene, quality, traceability and consumer confidence. Hygiene itself is a source of soft power because it builds trust.”

Reconnecting pilgrims at its core

The original Hejaz Railway was built chiefly to serve Muslim pilgrims traveling to Islam's holiest sites. Although freight and logistics dominate today's discussions, experts believe the passenger dimension could eventually become equally significant.

As Elmedawar notes, expanded connectivity could make Hajj and Umrah substantially more affordable, accessible, and environmentally sustainable.

"Easier rail travel would enable millions of Muslims from different countries to meet more frequently during Hajj and Umrah. In this way, the railway would connect not only cities but also people, cultures and shared values.”

Stumbling blocks

For all the optimism surrounding the initiative, the project faces enormous practical challenges. Bringing this vision to life requires synchronizing cross-border customs, digital freight systems, regulatory frameworks, and technical standards across multiple sovereign nations. The physical and financial obstacles are formidable. In Syria, rebuilding costs exceed $200 billion, with reconstruction focused on basic utilities rather than international rail, alongside ongoing security concerns.

Additionally, significant infrastructure gaps remain, including a missing 400-kilometer segment between Syria and Jordan that requires construction, and a $100 million restoration project needed to link Türkiye to Aleppo and Damascus, according to Elmedawar.

Financing these gaps presents another major hurdle. The total investment is estimated at $5.5 billion. While the Asian Infrastructure Investment Bank has committed $750 million to Turkish rail lines, a comprehensive cross-border funding model is still lacking.

As Elmedawar observes: "The principal constraint is no longer engineering. It is institutional coordination."

He suggests the Islamic Development Bank (IsDB) - a consistent backer of regional transport projects across the OIC - could provide the institutional framework necessary to unlock the corridor's full potential through direct financing, technical assistance, or institutional support.

Whether the project can be completed within the optimistic timeframe suggested by Turkish officials remains to be seen. But even at the memorandum stage, the railway signals an important change in regional thinking.

Governments increasingly view mobility projects as instruments for expanding geopolitical influence, fostering regional integration, and strengthening economic resilience. If political will and financial backing align, the Türkiye - Saudi corridor could catalyze a newly connected, economically resilient Islamic world.

But beyond the shattered infrastructure, the tipped over desks, the dangling wood beams and broken glass, another crisis has unfolded: a catastrophic shortage of digital equipment.

The conflict has decimated institutions, disrupted logistics, and triggered a strict blockade that predicates on the harsh understanding of labelling laptops, smartphones, and their spare parts as ‘dual-use’ military items. Securing tech in this new reality has become virtually impossible.

The context is both instructive and overwhelming: For millions around the world, a broken laptop is an inconvenience. In Gaza, it can mean the sudden demise of a university education, the loss of a family's primary income, or complete isolation from the outside world.

By cutting off access to technology, the blockade has suffocated daily life, disproportionately impacting students, remote workers, and a broader workforce desperate to link up with and serve the global economy.

“Gaza is facing an extreme, system-wide shortage of digital devices,” Maha Alfarra, managing director at the Galilee Foundation, a UK-registered charity focused on Palestinian education and humanitarian initiatives, tells Salaam Gateway.

Image Courtesy: Shutterstock

“Most laptops, tablets, and smartphones were destroyed during the war, and no new electronics have been allowed into Gaza since October 2023.”

The few devices that survive or slip through the blockade are priced astronomically. A basic laptop that once cost $400 now commands $1,000 or more. If a student's laptop breaks, they face an impossible choice: purchase a replacement at a hyper-inflated price or drop out entirely.

“Prices for the few remaining devices have risen to more than five times their original cost, far beyond the reach of most families and institutions,” Alfarra adds.

“At Al-Azhar University-Gaza, a recent $10,000 support fund was only enough to purchase five laptops, illustrating the scale of scarcity.”

Human capital, skillset at risk

The hardware shortage is triggering a much broader crisis: the erosion of Gaza's talent base and the demise of entire livelihoods.

Before the escalation, Gaza had fostered a resilient digital workforce. Through local incubators and university programs, young Palestinians built careers in software development, graphic design, and digital marketing, bypassing physical borders through the Internet. Today, those professionals are struggling to remain visible to global employers.

“Losing a laptop means losing an immediate economic lifeline or halting university progress entirely,” Wisam Elswerki, a Gaza-based content developer who works with humanitarian organizations, tells Salaam Gateway.

After losing his own equipment, Elswerki was forced to manage his workload entirely from a mobile phone. “Trying to handle professional documentation, join virtual meetings, and review files on a small screen - while dealing with erratic power and network coverage - turns standard work into a daily test of endurance.”

“A simple task takes four times longer than it should.”

Without the ability to work consistently, client relationships wither, and hard-earned technical skills inevitably decline.

“The greatest long-term risk is not the loss of laptops or smartphones - it’s the gradual loss of the human capital that took years to build,” Mohammed Abu Hassira, a development professional based in Gaza, tells Salaam Gateway.

Abu Hassira notes that before October 2023, remote work was one of the few accessible pathways to financial independence, particularly for women.

“Digital work depends on continuity,” he explains. “One of Gaza's greatest strengths has always been its people. Preserving digital talent and reconnecting professionals with global markets should therefore be viewed not only as humanitarian support, but as a strategic investment in Gaza's long-term economic recovery.”

In the face of these extreme restrictions, Palestinians are engineering makeshift solutions using damaged equipment and pre-digital adaptations.

When laptops and computers are unavailable, students use mobile phones to access course materials on platforms like Moodle or Google Classroom, relying on WhatsApp as their primary tool for peer-led engagement.

Families frequently pool their resources, sharing a single rented laptop among multiple siblings just to keep their education alive. Tech workers and freelancers travel through destroyed neighborhoods to reach makeshift, solar-powered co-working hubs. There, they share access to electricity to charge devices, rotating in shifts to maintain their income streams.

“Despite severe logistical restrictions, several organizations have launched creative initiatives to restore digital access,” Elswerki notes.

He highlights entities like Gaza Sky Geeks and Taqat Gaza, which have been instrumental in setting up community tech spaces, as well as Academic Solidarity with Palestine, an initiative distributing free e-SIMs to help Gazan students and professors re-establish basic connectivity.

“While the gap between supply and demand remains massive, these efforts keep Gaza's workforce and student body connected,” he says.

Integrated ecosystems are the sole way forward

Standard charity models are no longer viable in an environment stripped of basic power and connectivity.

“Companies can play a meaningful role, but only if support goes beyond simply donating devices,” warns Alfarra. “In Gaza’s current conditions, digital access depends on three things simultaneously: devices, power, and connectivity. Effective programs therefore need to be integrated and resilient.”

To build these ecosystems, international bodies are shifting their focus from individual distribution to shared resources. Rather than dropping single laptops into an infrastructural vacuum, they are now equipping collective workspaces.

Investing in decentralized, solar-powered computer labs and coworking spaces allows hundreds of people to use reliable equipment through shift schedules. UN agencies such as UNESCO and the UNDP have already piloted similar approaches.

“UNESCO has provided laptops through Temporary Learning Spaces, supporting more than 10,000 students, while UNICEF continues to procure ICT equipment for Palestinian education systems," Alfarra says.

"Furthermore, a major initiative led by Education Above All and UNDP distributed 10,000 tablets and built 100 digital learning centres equipped with reliable power and internet access.”

Other NGOs - including US-registered HEAL Palestine, West Bank-headquartered Teach for Palestine and US-based GiveInternet - have contributed crucial hardware, connectivity tools, and remote learning assistance. These initiatives prove that progress is possible when device distribution is paired with infrastructure and training.

Preserving the future

The Galilee Foundation raised around £106,000 in a campaign to fund laptops and tablets for Gaza. However, with electronics barred from entering the Strip, the charity is pivoting toward high-impact, locally informed strategies.

“We’re now assessing where our support can be most effective within this ecosystem,” says Alfarra. “We’re comparing three interventions: device handouts, shared access hubs, and digital classroom platforms. Early evidence suggests that shared hubs combined with digital platforms offer the greatest impact under current constraints.”

To truly unlock online access, Alfarra asserts that stakeholders must coordinate hardware grants alongside low-cost rental models. This framework should offer communities flexible ways to secure refurbished computers from the secondary market, such as borrow-and-return schemes or installment plans.

Citing mechanisms outlined by Al-Azhar University, she argues that organizers must keep distribution targeted, prioritizing financially disadvantaged students and professionals whose specialized fields - such as engineering or software development - simply cannot be managed on mobile devices.

Meanwhile, international clients and academic institutions must adapt to the constraints facing these professionals, adds Elswerki. This requires optimizing platforms to be low-bandwidth and mobile-first, ensuring essential web tools run smoothly on basic mobile browsers.

Ultimately, overcoming the technological blockade is less a logistical challenge than a humanitarian imperative to preserve an entire generation’s future.

“Rebuilding Gaza's digital economy goes beyond replacing damaged devices,” notes Abu Hassira.

“It’s about protecting decades of human capital and empowering skilled individuals to reconnect with education, employment, entrepreneurship, and global markets. Investing in digital access today is an investment in Gaza's most valuable asset - its people.”

We're growing — and want you to be part of our journey

Salaam Gateway has always been your home for independent, in-depth coverage of the global

Islamic economy. To help us go deeper and do more, we're introducing a membership tier for

our premium reports and insights — so we can produce more of everything you've come to love.

Elsayed: By being verifiable rather than loud. We don't chase the biggest number — we publish only what we can evidence. The certificate of analysis is the heart of it: a customer doesn't have to take our word on potency, they can see the independent lab result. I'd rather state an honest, verified 2.67% thymoquinone than an unverifiable higher figure. In a category criticised for weak regulation, transparency is the product.

Elsayed: By being verifiable rather than loud. We don't chase the biggest number — we publish only what we can evidence. The certificate of analysis is the heart of it: a customer doesn't have to take our word on potency, they can see the independent lab result. I'd rather state an honest, verified 2.67% thymoquinone than an unverifiable higher figure. In a category criticised for weak regulation, transparency is the product.