Bond record, budget pain, Iran and Biden: Mideast risks in 2021

Published 22 Dec,2020 via Bloomberg Markets - Gulf Arab nations approach 2021 with their currency pegs steadied, oil prices clawing back ground, and bond investors keen for the region’s high-rated, high-yielding names.

But the pain from Covid-19 and the slump in crude hasn’t gone, and S&P Global Ratings predicts only a “modest recovery” in the six-nation Gulf Cooperation Council through 2023, after a contraction of about 6% this year. And while the region’s markets are used to geopolitical ructions, investors are waiting to see how Joe Biden’s presidency might tilt the picture, according to Tarek Fadlallah, the Dubai-based chief executive officer of the Middle East unit of Nomura Asset Management.

Here are some of the themes investors will be watching in the Gulf:

Bond Binge, Part 2

Governments and companies in the GCC will issue about $120 billion of dollar debt and Islamic securities in 2021, according to Franklin Templeton. That compares with a record $127 billion this year.

The United Arab Emirates will dominate corporate sales, with Saudi Arabia and Qatar leading among sovereign issuers, said Mohieddine Kronfol, Dubai-based chief investment officer for Middle Eastern and North African fixed income at Franklin Templeton. Kuwait will be a “large contributor” to the region’s offerings if it renews a debt law that lapsed after its debut Eurobond issuance in 2017, Kronfol said.

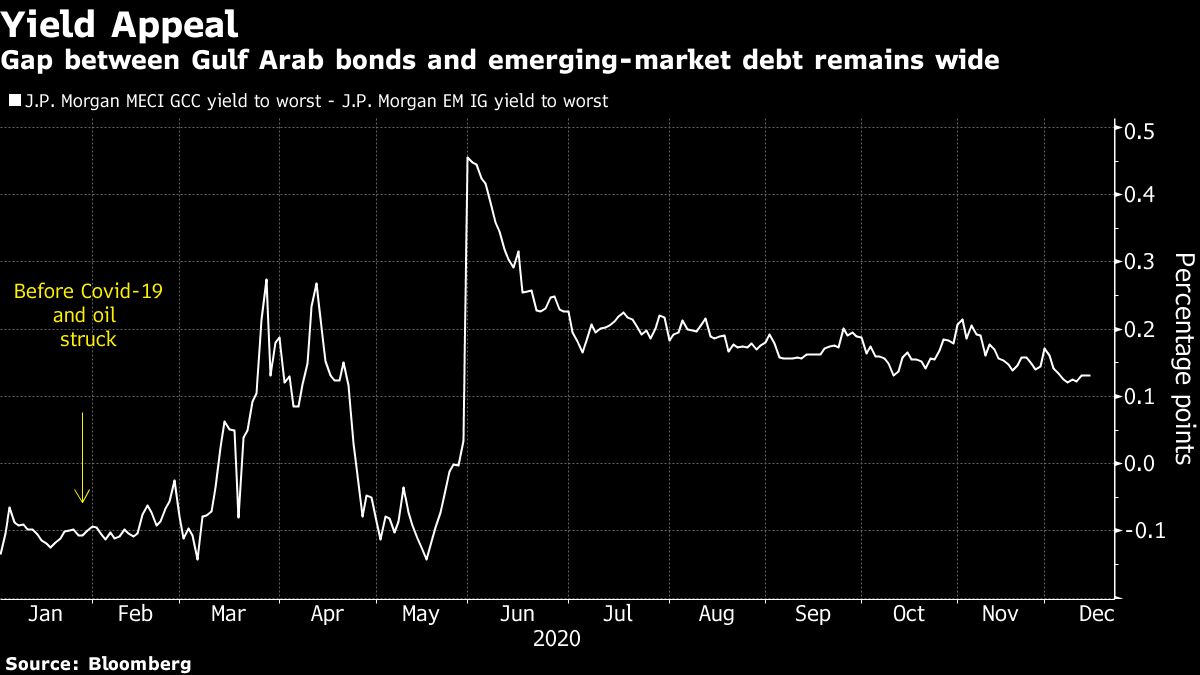

In addition, Fitch Ratings forecasts more than $40 billion in local-currency bond placements, mostly in Saudi Arabia. Gulf Arab dollar bonds outperformed emerging-market peers with a gain of more than 8% this year.

Weak Links

For the shakier economies in the Gulf, budget frailty could lead to a social backlash.

“Balance sheets will continue to deteriorate,” said Krisjanis Krustins, a Hong Kong-based director at Fitch Ratings. “Deficits will remain sizable, particularly in the lower-rated oil exporters and Kuwait, leading to continued deterioration of sovereigns’ debt and net foreign asset metrics.”

Bahrain and Oman, the region’s weakest links, are borrowing and possibly seeking support from wealthier neighbors. In Kuwait, the government has almost exhausted its liquid assets, leaving it unable to cover a budget deficit expected to reach the equivalent of almost $46 billion this year.

Nomura’s Fadlallah said he’s concerned how the relatively new leadership in Kuwait and Oman will navigate a “particularly challenging period of fiscal reform.”

No Bargain

For the most part, equities in the region are expensive compared with those of other developing nations and it will be local investors that set the markets’ direction rather than foreign flows, said Hasnain Malik, the Dubai-based head of equity strategy at Tellimer.

At the same time, stocks in Qatar benefit from the nation’s resilient fiscal position, and Dubai and Egypt have comparatively appealing valuations, Malik said.

The Biden Factor

The incoming administration could potentially reinstate the 2015 Iran nuclear deal that Donald Trump ditched.

Under Trump, officials brokered an accord normalizing Israel’s relations with the UAE and Bahrain that has raised investor hopes for an easing of tensions in the region. He’s also prodded Saudi Arabia and Qatar toward a preliminary deal to end their more than three-year rift.

Bond markets would see a short-term, limited impact from geopolitical developments, said Abdul Kadir Hussain, the head of fixed-income asset management at Arqaam Capital in Dubai.

“It is a constant risk factor in these parts,” he said. “The main drivers for the regional bond markets will continue to be the virus, central bank accommodation and supply.”

For more articles like this, please visit us at bloomberg.com

©2020 Bloomberg L.P. All Rights Reserved. Provided by SyndiGate Media Inc. (Syndigate.info)

DISCLAIMER: This content is provided to us “as is” and unedited by an external third party provider. We cannot attest to or guarantee the accuracy of information provided in this article from the external third party provider. We do not endorse any views or opinions included in this article.