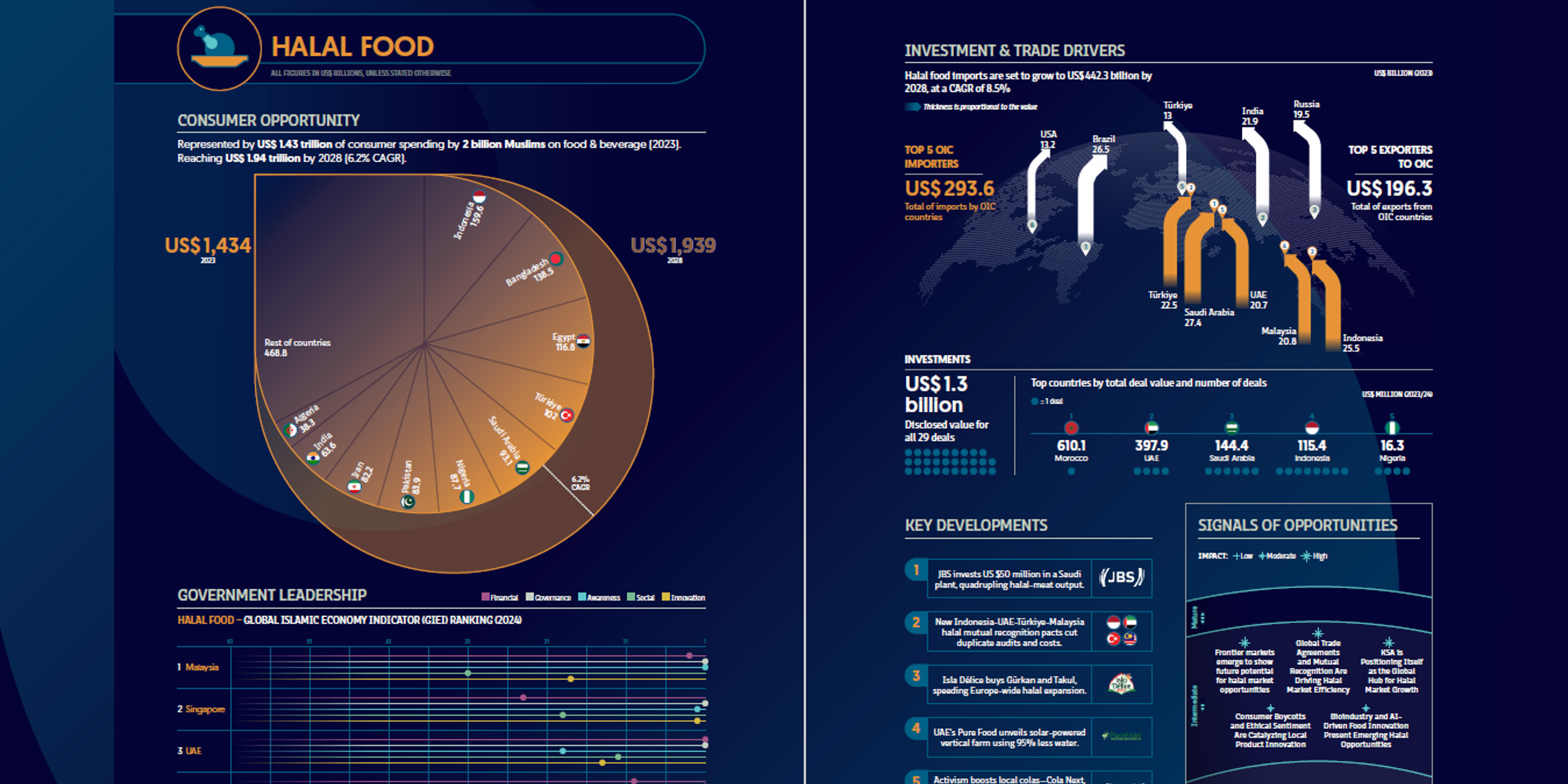

The halal-food market continues to anchor the wider Islamic economy. Muslim consumers spent US $1.43 trillion on food and beverages in 2023; buoyed by population growth, localisation of production and stronger certification regimes, spending is expected to reach US $1.94 trillion by 2028, a healthy 6.2% CAGR. Indonesia remains the single largest national market by expenditure, followed by Bangladesh and Egypt.

Trade flows are accelerating even faster than consumption. OIC members imported US $293.6 billion of halal-related food in 2023 and are set to lift that bill to US $442.3 billion by 2028, implying 8.5% annual growth. Saudi Arabia, Türkiye, Indonesia, Malaysia and the UAE are the five biggest buyers inside the bloc, while Brazil, India, Russia, Türkiye and the United States supply the largest export volumes into OIC markets. Government-to-government mutual-recognition agreements (such as the new Indonesia–UAE–Türkiye–Malaysia pact) are shaving certification costs and widening market access.

Investor appetite cooled in value terms last year, yet remained significant: 29 disclosed halal-food deals totalled US $1.3 billion. Morocco topped the league by ticket size thanks to a US $610 million sugar acquisition, followed by the UAE (US $398 million), Saudi Arabia (US $144 million), Indonesia (US $115 million) and Nigeria (US $16 million). Activity centred on capacity expansion—Brazil’s JBS poured US $50 million into a Saudi processing plant to quadruple output, while UAE conglomerates are investing in vertical farming to slash water use.

Free, in under 30 seconds

Join thousands of professionals reading Salaam Gateway — the Global Islamic Economy Gateway.

Already a member? Sign in

- 5 free articles every month

- Weekly Islamic-economy newsletter

- Save articles to read later