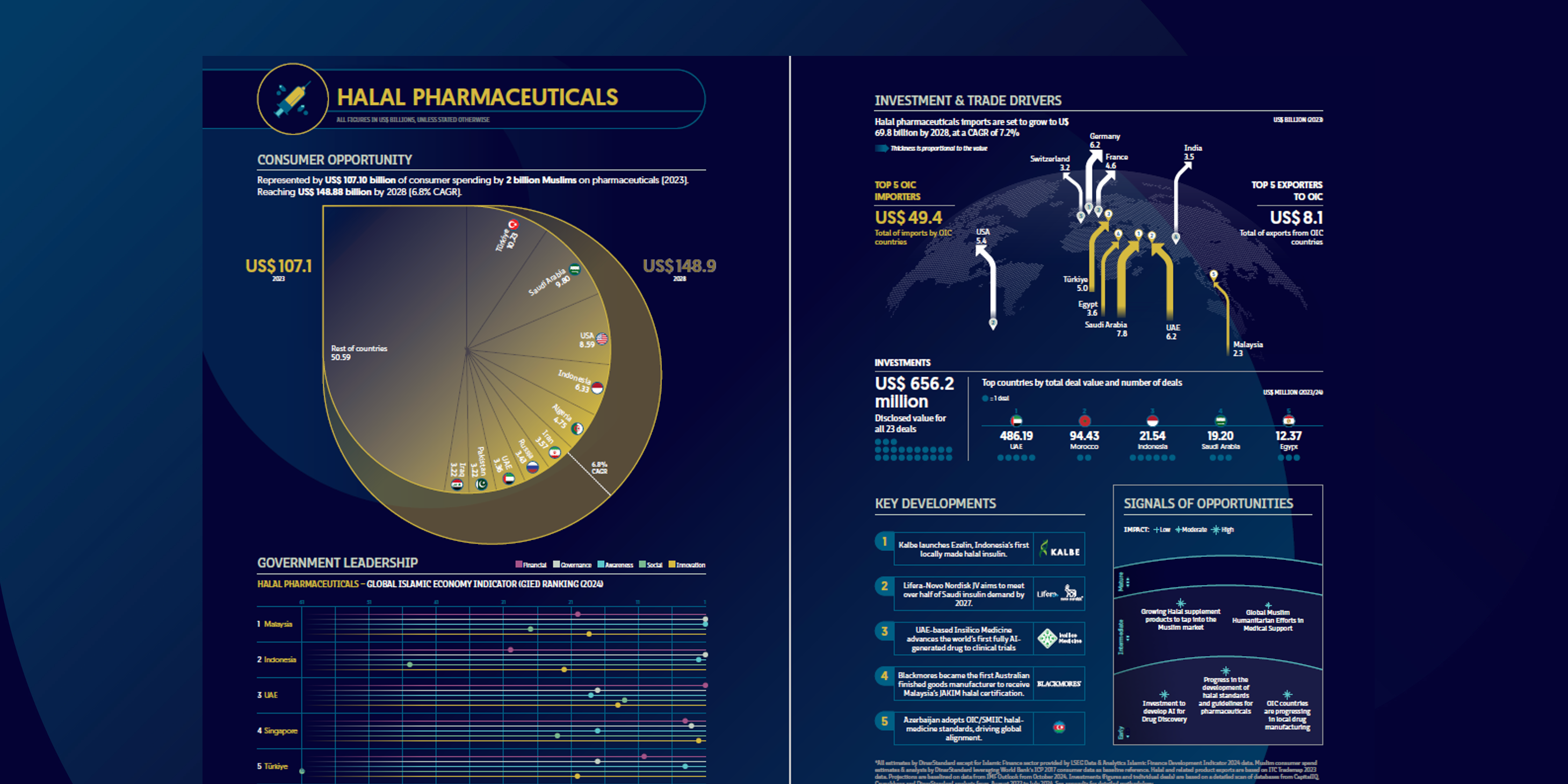

Muslims spent an estimated US $107 billion on medicines and health-related products in 2023. As certification frameworks mature and frontier markets localise production, outlays are projected to reach US $149 billion by 2028, equivalent to a 6.8 % compound annual growth rate. Turkey, Saudi Arabia and Iran remain the three largest end-markets, while Indonesia, Malaysia and Egypt are the fastest climbers in absolute demand.

Trade & investment pulse

Continue reading

Free, in under 30 seconds

Join thousands of professionals reading Salaam Gateway — the Global Islamic Economy Gateway.

Joined by 12,000+ Islamic economy professionals

Create a free account

Already a member? Sign in

- 5 free articles every month

- Weekly Islamic-economy newsletter

- Save articles to read later