Islamic Finance Sector Snapshot 2024/25

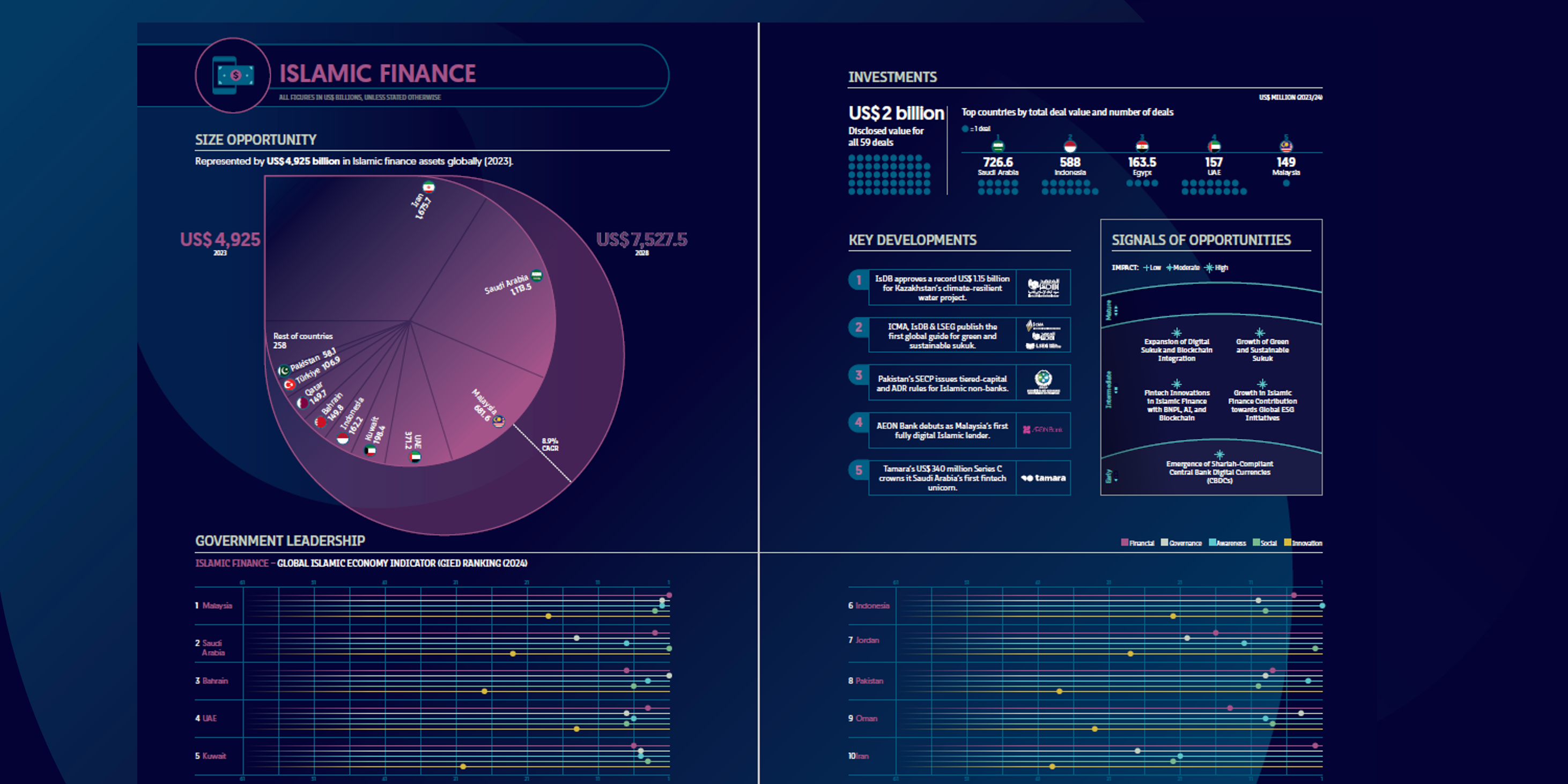

Islamic finance remains the chief engine of capital for the broader halal-economy ecosystem. Total Shariah-compliant assets reached US $4.93 trillion in 2023; on current trajectories they are forecast to expand to US $7.53 trillion by 2028, implying a robust 8.9 % compound annual growth rate. Saudi Arabia anchors the industry with just over US $1 trillion in assets, followed by Iran, Malaysia, the UAE and Qatar, which together account for well over two-thirds of global market share.

Investment Pulse

Continue reading

Free, in under 30 seconds

Join thousands of professionals reading Salaam Gateway — the Global Islamic Economy Gateway.

Joined by 12,000+ Islamic economy professionals

Create a free account

Already a member? Sign in

- 5 free articles every month

- Weekly Islamic-economy newsletter

- Save articles to read later