Media & Recreation Sector Snapshot 2024/25

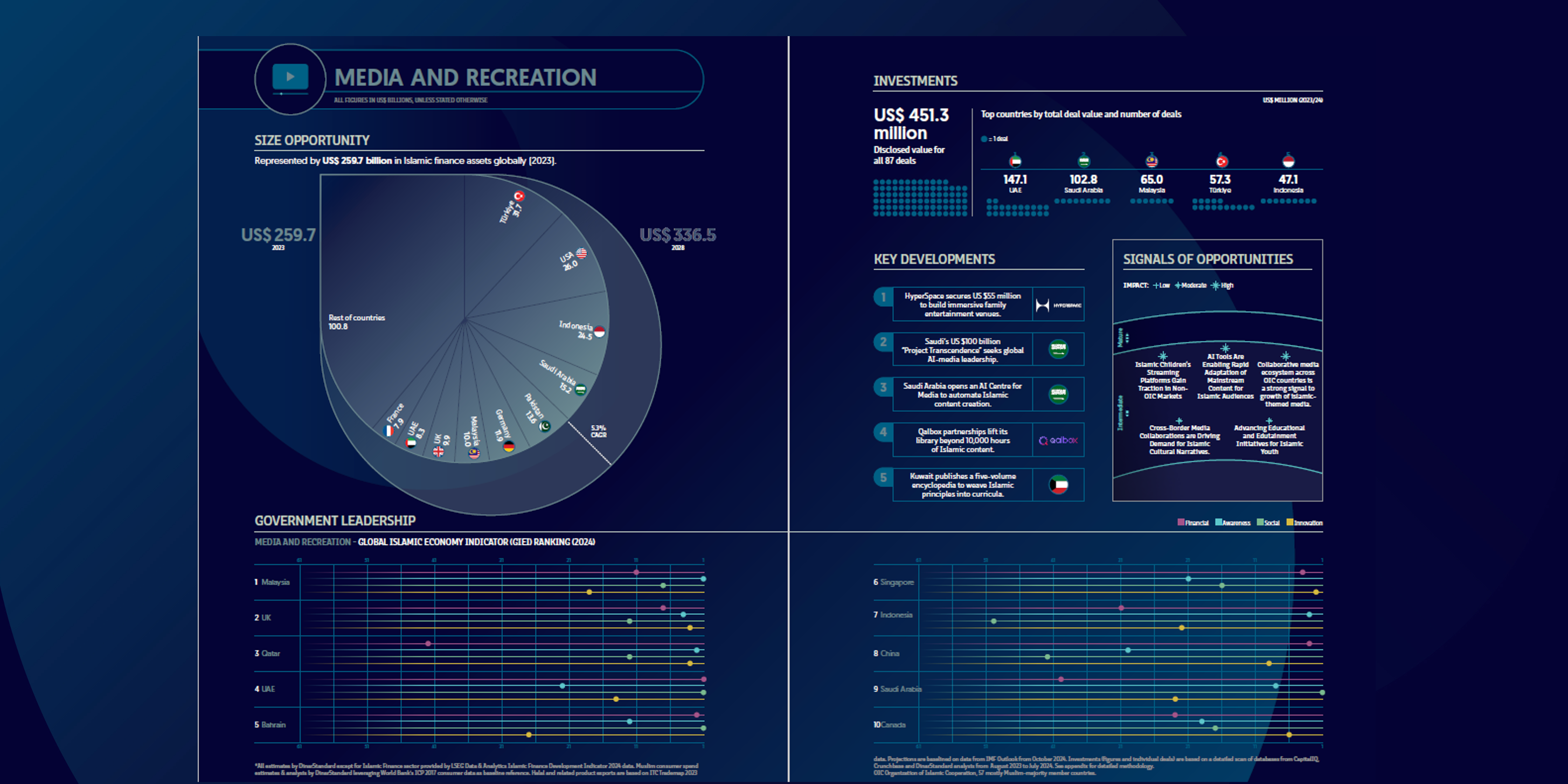

Muslim audiences spent US $259.7 billion on media and recreation in 2023; as digital-content consumption accelerates, that figure is expected to rise to US $336.5 billion by 2028, a 5.3 % CAGR. The largest single markets are Türkiye (≈ US $31.7 bn), the United States (US $26 bn) and Indonesia (US $24.5 bn), while Saudi Arabia, Pakistan and Germany form the next tier; a long “rest-of-world” tail still accounts for more than US $100 bn, signalling room for new entrants.

Investment pulse

Continue reading

Free, in under 30 seconds

Join thousands of professionals reading Salaam Gateway — the Global Islamic Economy Gateway.

Joined by 12,000+ Islamic economy professionals

Create a free account

Already a member? Sign in

- 5 free articles every month

- Weekly Islamic-economy newsletter

- Save articles to read later