Nigerian fintech TeamApt working on non-interest financing for SMEs

TeamApt, a leader in Nigeria for payment infrastructure and digital banking, is working on tech for non-interest financing for small businesses in the north of the country.

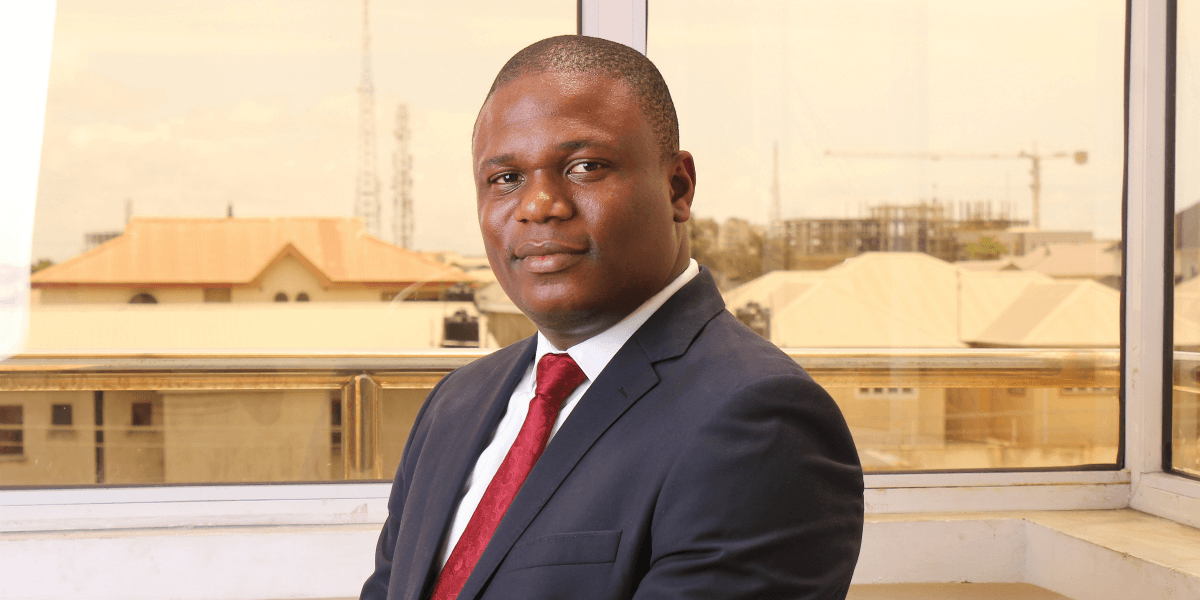

“We expect to have banking partnerships to bring the product to life,” Tosin Eniolorunda, founder and CEO of TeamApt, told Salaam Gateway. The company plans to launch the product in the coming quarters after regulatory approvals.

Nigeria’s bustling fintech scene raised more than $600 million in funding the past five years. In 2019 alone, the West African nation attracted a quarter of the $491.6 million solicited by African tech start-ups and is now home to over 200 fintech standalone companies.

Free, in under 30 seconds

Join thousands of professionals reading Salaam Gateway — the Global Islamic Economy Gateway.

Already a member? Sign in

- 5 free articles every month

- Weekly Islamic-economy newsletter

- Save articles to read later